Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

Why Living Abroad For Six Months Doesn’t Automatically Mean You’re No Longer An Australian Tax Resident

Daniel Wilkie | 19 Jan 2021 | 5 min read

When it comes to tax residency, the six month rule is quite simple to understand: live in a country for at least six months, or 183 days, and you’re considered a tax resident of that country.

The simplicity in this rule explains why it is a common way of determining when an individual taxpayer is considered to be a tax resident of the country they are living in. In fact, for some countries, this is exactly how they determine tax residency.

For this reason it can be natural to assume that if you live overseas for at least six months then you are a tax resident of that country and no longer a tax resident of Australia. This is particularly the case if that country specifically states that they consider you to be a tax resident when you are living in their country for at least six months.

See here for a brief overview of the key differences between a Permanent Resident and Temporary Resident.

Why You May Still Be Considered An Australian Resident While Living Overseas

If you are an Australian citizen then Australia is your default home country in relation to tax residency. This means that it’s not just about meeting the tax requirements of the other country to be classed as a foreign tax resident for Australian tax purposes.

Under Australian tax laws an Australian citizen, who has been living as a tax resident, continues to be an Australian tax resident until they make a permanent move overseas. A permanent move overseas requires them to effectively cut ties with Australia. Typically the move overseas must be for a minimum of two years, and you must be setting up a permanent home in your new country (not just travelling around, or staying in hotels).

The Impact Of Double Tax Agreements

A double tax agreement (DTA) between two countries may contain provisions that help determine which country has taxation rights when an individual’s tax residency status is not clear cut.

For example, this might happen when an individual goes to a country that treats them as a tax resident after six months living there, however, under Australian tax laws they are also still treated as a tax resident. The DTA, through the tie-breaker provisions, helps determine in which country the individual taxpayer should be treated as a tax resident.

DTA typically gives weight to the country where the person has their permanent home, by virtue of birth or choice. In practice this means there is an expectation that the country in which an individual is a citizen, particularly if they clearly intend to return to their home country, retains more rights than a country they are temporarily living in. Beyond this, DTAs tend to consider where an individual’s personal and economic ties are stronger.

Unclear Situations

Most people find themselves in clear situations. They are either an Australian tax resident or a foreign tax resident, based on the country that they are a permanent resident. However, since individual circumstances can be very unique, there are plenty of situations that are not so clear cut.

Consider a situation where an individual lives in multiple countries, moving from one to another through the year. Or there are situations where an individual moves to one country, intending to remain there permanently, only for an unexpected issue to arise that results in them changing their mind and relocating to another country.

The Pandemic

COVID-19 has resulted in many people staying in countries for significantly longer periods than they ever planned. Conversely, many Australian expats have returned home to Australia to ride out the pandemic, despite previously intending to remain living overseas.

Since each situation is different, it is impossible to give clear, generic advice on these grey areas. The special circumstances of COVID-19 mean that even some Australians who were holidaying overseas have been unable to return home to Australia as planned. Their time overseas does not automatically cause them to become a foreign tax resident, especially where their intent and actions remain to return to Australia as soon as they are able to.

Others who have been living overseas for many years have returned to Australia for a prolonged period due to the pandemic. Their time in Australia does not automatically mean they resume Australian tax residency, however this requires them to be intending to return to the country they consider home as soon as possible. As the pandemic continues, it becomes more difficult to ascertain what “as soon as possible” means, and what actions would indicate a change in circumstances and intent.

Six Months Living Overseas

We cannot treat six months living overseas as automatically resulting in a change of tax residency. It should be understood that a change of tax residency will only occur if an Australian moves overseas for a period no shorter than six months, and a permanent place of abode is established. The subtle difference means that a stay of less than six months can clearly be understood to be temporary and would not change tax residency, while an overseas move that is expected to last more than six months requires review to determine if, and when, there is an actual change in tax residency.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

UK Budget 2024 – Non-UK Domiciled Tax Rules To Be Scrapped

27th Mar 2024

Richard Feakins

The current remittance basis tax regime will be replaced by a residence based regime from 6 April 2025 Foreign Income And Gains Existing non domiciled individuals who have been resident in the...

Moving Overseas: Tax Consequences Of Keeping Or Selling Your Australian Main Residence

11th Mar 2024

Matthew Marcarian

Leaving Australia means leaving your home Unless you’re intending to return to Australia in the foreseeable future, this means deciding whether you want to keep or sell that property When...

This year has seen the ATO crack down on individuals who have been trading in cryptocurrencies, such as bitcoin. This is a reminder for those dealing in such transactions to be well aware of the taxation obligations that come about with any resulting financial gains and losses. It is imperative to ensure accurate and complete cryptocurrency tax reporting.

How the ATO considers Cryptocurrency

Cryptocurrencies are considered by the ATO to be a form of property and are therefore a CGT (capital gains tax) asset for tax purposes.

As is the case with any asset that is subject to capital gains tax, it is necessary to maintain detailed records of transactions, including receipts of purchase or transfer, exchange records, digital wallet records and keys, as well as the value of the cryptocurrency in Australian dollars at the time of the transaction.

Transactions with Cryptocurrency during a CGT Event

Typically, a CGT event will occur when a cryptocurrency is sold, gifted, traded, converted to a fiat currency (such as Australian dollars) or used to obtain goods or services. Given the number of cryptocurrency transactions subject to tax, it is a danger that some of these could unwittingly slip through the cracks, so tax implications must be kept in mind whenever transacting with cryptocurrency for any purpose.

Conversely, it is also important to consider whether the cryptocurrency has been purchased for personal use (as opposed to any profit-making endeavour), as this is will exempt it from capital gains tax.

An exception arises to the treatment of cryptocurrency as a CGT asset when it is held as trading stock, or is used for business transactions. In these cases, it is considered to be held on revenue account, and its value in Australian dollars will be included as part of an entity’s ordinary income. That means that either normal personal tax rates will apply, or normal business tax rates will apply.

Tracking Cryptocurrency Transactions

Record keeping for cryptocurrency transactions may appear to be burdensome and unclear at times but there are a number of resources available to assist us, including official online exchanges which offer reliable Australian dollar values of the cryptocurrency at the time of transaction.

Individuals who have traded cryptocurrencies of any amount should ideally have a system in place to track these, as the ATO has shown that it will not overlook even the most seemingly small or insignificant transactions.

CST can assist clients who trade or invest in cryptocurrencies as part of their broader investment activities.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

This Federal Budget has been shadowed by the economic uncertainty and unusual difficulties faced under the coronavirus. This means there has been a general expectation that there would be significant announcements made in the effort to stem the negative impact that COVID-19 restrictions have had on the economy.

With the income tax changes covered in the Treasury Laws Amendment (A Tax Plan for the COVID-19 Economic Recovery) Bill 2020 passing both houses of Parliament on 9 October 2020, both employers and employees could be seeing the benefit of budget announcement in a matter of weeks.

Here’s an overview of the key Government announcements.

Personal Income Tax

The planned reduction in personal income tax rates is being brought forward to 1 July 2020. That means you’ll be seeing the benefits not just in your 2021 tax return, but in adjustments to your salary package as soon as the PAYGW rates are updated.

While the tax free threshold and the top marginal tax tier remain unchanged, the 19%, 32.5%, and 37% tax tiers now cover higher levels of income.

*

Previous Tax Rate for 2021

New Tax Rate for 2021

NIL Tax

0-$18,200

0-$18,200

19% Tax

$18,201-$37,000

$18,201-$45,000

32.5% Tax

$37,001-$90,000

$45,0001-$120,000

37% Tax

$90,001-$180,000

$120,001-$180,000

45% Tax

$180,001 +

$180,001+

*Medicare levy of 2% also applies unless exempt.

Low Income Tax Offset (LITO) and Low and Medium Income Tax Offset (LMITO)

The LMITO offset of a maximum of $1,080 for taxpayers will continue to apply in the 2021 income tax year. Individuals with a taxable income of between $48,000 and $90,000 will be able to access this offset in full.

The maximum low Income Tax Offset is increased to $700 for individuals earning under $37,500. A pro-rata amount of the low income tax offset will be available to individuals who earn under $66,667. (The LMITO is also available to low income tax earners in addition to the LITO).

Instant Asset Write-Offs

Unlike previous allowances for instant asset write-offs, this allowance is uncapped. That means eligible businesses can claim the full cost of new assets purchased, regardless of how much those purchases were.

From 7:30pm 6 October 2020 until 30 June 2022 the instant asset write off provisions have also been extended to businesses with a turnover of up to $5 billion.

This will essentially mean that 99% of businesses will be able to fully write off the cost of purchasing and installing assets that are acquired and first used between 7 October 2020 and 30 June 2022.

Small businesses (under $10 million turnover) with a balance in a simplified depreciation pool, will be able to expense the full remaining balance of that pool in the 2021 and 2022 years.

Loss Carry-Back

For businesses with a turnover of up to $5 billion who have made a tax loss this year, but paid taxes in previous years, the government is creating an opportunity to go back and offset current losses against previous profits. This will allow those businesses to generate a refund from those previously paid taxes.

The limitations imposed on this measure include:

Limiting the amount carried back to be no more than the earlier taxed profits.

The requirement that the carry-back does not cause a company to have a franking account deficit.

The tax refund generated by carry-back losses will be available to eligible businesses on lodgement of their 2021 and 2022 tax returns. As this measure is optional, businesses can choose to simply carry forward their current year tax losses as normal.

Small Business Tax Concessions Extended to Larger Businesses

The small business tax concessions have been extended to businesses who have an aggregate annual turnover of between $10 million and $50 million.

Access to small business tax concessions include:

From 1 July 2020, eligibility to immediately deduct certain start-up and prepaid expenses.

From 1 April 2021, exemption from the 47% FBT on car parking and multiple work-related portable electronic devices (phones, laptops) being provided to employees.

From 1 July 2021, access to simplified trading stock, PAYGI remittance based on GDP adjusted notional tax, and monthly settlement of excise duty.

A two year amendment period for assessments from 1 July 2021.

Potential for a simplified accounting method for GST purposes.

JobMaker Incentive

The JobMaker incentive is a government grant paid to employees who hire young job seekers.

The payments are made at $200 a week for eligible employees between 16 and 29 years old, or $100 a week for eligible employees between 30 and 35 years.

The limits and eligibility criteria include:

The job must be a newly created job between 7 October 2020 and 6 October 2021. It must not displace an existing employee.

The credit is claimed quarterly in arrears and is capped at $10,400 for each new position created.

The credit claimed cannot exceed the payroll increase for the reporting period.

Eligible employees must be paid for a minimum of 20 hours per week on average over the reporting period

The new employee must have been on JobSeeker, Youth Allowance, or Parenting Payments for at least one out of the past 3 months before being hired.

The new employee cannot be an existing or former employee of the business and the employer cannot also be receiving a wage subsidy under another program for the employee.

Employers claiming JobKeeper payments are not eligible.

New employers created after 30 September 2020 will not be able to claim for the first employee they hire.

R&D Incentives

Small companies with turnovers below $20 million will have access to an 18.5% R&D tax offset.

Corporate Residency Test

Where a company was incorporated offshore it now has a chance to be considered an Australian tax resident. To become an Australian tax resident the company must have “significant economic connection to Australia”. This effectively means that the company must undertake their core commercial activities in Australia and have its central management and control in Australia.

Keeping up with technology

While not strictly a tax measure, the Government has also indicated that they will be looking into making permanent changes to the Corporations Act 2001 in order to keep up with the times. This would mean companies could achieve a quorum through virtual attendance at meetings and provide certainty on issues such as electronically executing documents.

FBT Changes

A new FBT exemption will be introduced for employers to retrain and reskill employees who are being made redundant. This is so that the employer can help reskill an employee for a brand new position without triggering an FBT liability in covering costs that don’t have a sufficient connection to their existing role. This does not cover the cost of Commonwealth supported university placements or repayments of Commonwealth student loans.

The Government is also looking at measures to reduce the compliance burden on FBT returns being finalised from 1 April 2021.

CGT on “Granny Flats”

Where an elderly or disabled person transfers their home, or the proceeds from the sale of their home to an adult child or trusted person, so that the trusted person can provide ongoing housing and care for them, then a CGT exemption will be applied to the arrangement.

Commercial rental arrangements are not covered by this exemption. It only applies where the arrangement is entered into on the basis of family relationships or other close personal ties.

Taxing Times

With many concessions, rate changes, incentives, and ease of administrative burden efforts under way, taxpayers could be seeing a large overhaul that may leave a permanent mark on the tax system.

Please keep in mind that the announcements are subject to change as the Government finalises legislation.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

Australian Moving to the UK: How Do I Treat Non-UK Sourced Income?

Daniel Wilkie | 15 Sep 2020 | 6 min read

One of the top questions we are asked by Australians who are moving to the UK, is “how am I taxed on my non-UK sourced income in the UK?”

Since a UK non-resident would only be taxed on any UK sourced income, this question is predicated on the basis that the Australian is moving to the UK on a permanent basis. A permanent move means that they are ceasing to be an Australian tax resident and instead will be considered a UK tax resident.

In general, just like Australia, the UK taxes residents on their worldwide income. This means that UK tax residents have to pay tax on any income they earn, regardless of where the income is sourced. However, there is a clause for what they consider “non-domiciled” residents, whereby taxes are instead paid on a remittance basis. Since many Australians moving to the UK would fall into the definition of a “non-domiciled” resident, this is an important question. We cover what this means below.

Australian Tax Rules on Non-Australian Sourced Income

For comparison, let’s consider the Australian rules on residency. Most people are aware that as an Australian tax resident you are required to pay Australian income tax on income you receive, regardless of where it is sourced. However there are certain exceptions for individuals who are temporary residents. Once you cease to be an Australian resident you are only required to pay Australian income tax on income that has an Australian source.

The UK operates on a similar basis, however their exemption for “temporary” residents is measured and treated differently than Australia’s exemption.

UK Residency Rules

In general, tax residents of the UK are liable for income tax in the UK, on their worldwide income. This means that it doesn’t matter where the income is sourced, it is included in the resident’s tax return.

In the UK you are automatically considered a tax resident when either one of of the following applies:

You spend over 183 days in the UK during the tax year.

Your only home was in the UK (owned, rented or lived in for at least 91 days, with at least 30 days spent there in the tax year).

Conversely you are automatically considered a non-resident if either of the following applies:

You spent under 16 days in the UK (or 46 if you haven’t been classed as a UK resident for the previous 3 tax years).

You worked on average 35 hours a week abroad, and spent less than 91 days in the UK, of which less than 31 days you were working in the UK.

Keep in mind that in instances where an individual would be considered dual tax residents of Australia and the UK, then the tie breaker rules in the Double Tax Agreement require consideration to determine which country has taxing rights on the different sources of income.

However, while the general rule is that tax residents are assessed on their worldwide income, there is, as indicated previously, an exception. This exception is for tax residents whom the UK considers to be “non-domiciled residents”.

Non-domiciled UK Residents

Non-domiciled residents are individuals, including Australian citizens, who are only living in the UK for the short to medium term.

A UK resident who has a permanent home outside of the UK is considered to have a domicile in that other country. This doesn’t necessarily have to be a specific, physical house, but more so that the ties to their home country mean that this country is considered to be their ‘permanent’ home. When an individual has a permanent home outside of the UK they are considered to be a “non-domiciled” tax resident of the UK.

In the UK a ‘domicile’ is typically the country in which your father permanently resided when you were born. For instance, the country in which you are a citizen by descent. However, this may not be the case if you have legitimately and permanently moved to another country, with no intention of returning to your original home country. This would mean that your ‘domicile’ changes to the new country in which you begin to permanently reside.

“Remittance” Rules on Taxes on Non-UK Sourced Income for Non-domiciled Residents

For non-domiciled residents, non-UK sourced income is treated differently depending on the total amount of the non-Uk sourced income.

Under 2,000 Pounds

If you are a “non-domiciled” UK resident then you ignore all foreign income and gains if that income is under 2,000 pounds for the tax year and you do not bring that income into the UK. You must have a bank account in your home country, and the funds from that income must stay back in the home country instead of being transferred into the UK. If this is the case then you don’t have to do anything about your foreign income when lodging a tax return.

However, if the income you earn from overseas sources exceeds 2,000 Pounds, or you bring any income into the UK, then you must report that income in a self-assessed tax return.

Over 2,000 Pounds

When the non-UK sourced income exceeds 2,000 pounds (or the income is brought into the UK), the income can’t just be ignored. The rules under which foreign income is taxed in the UK, for non-domiciled residents, is the ‘remittance basis’. This essentially means that you have a choice on how you treat the reported income.

Choice of how UK Taxes are Sorted Out

Choice 1: You can Simply Choose to Pay UK Taxes on the Income.

If you choose this option then you will be assessed for income tax on your foreign income. If tax is paid on the Australian sourced income (or may be taxed elsewhere if it is income relating to another country), there are a number of rules that ensure you are not taxed twice on this income. In some cases this will result in a reduction to your UK taxes.

Choice 2: You can Claim the ‘Remittance Basis’.

If you choose to be taxed on the remittance basis, then you only have to pay tax on any of the income that you actually bring into the UK.

However, in a trade off for this consideration, you will lose any tax-free allowances for income tax and capital gains. You will also be required to pay an annual charge if your residency in the UK exceeds a certain timeframe. This annual charge is 30,000 pounds if you have resided in the UK for at least 7 of the past 9 years, or 60,000 pounds if you have resided in the UK for at least 12 of the past 14 years.

The remittance basis may be a great option if you are living in the UK for less than 7 years, however, beyond this you would need to assess your situation to determine your optimal position.

Seek Appropriate Advice for your Situation

Since the remittance basis can get complicated it is best to talk to a UK tax adviser for specific advice. You need to consider your own position, your long term intentions, and where you hold your investments, including rental properties, that are generating taxable income.

See here for a brief comparison of the Australian and UK tax system.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

UK Budget 2024 – Non-UK Domiciled Tax Rules To Be Scrapped

27th Mar 2024

Richard Feakins

The current remittance basis tax regime will be replaced by a residence based regime from 6 April 2025 Foreign Income And Gains Existing non domiciled individuals who have been resident in the...

Moving Overseas: Tax Consequences Of Keeping Or Selling Your Australian Main Residence

11th Mar 2024

Matthew Marcarian

Leaving Australia means leaving your home Unless you’re intending to return to Australia in the foreseeable future, this means deciding whether you want to keep or sell that property When...

Australian Expats Living In The USA: Understanding Your Investment Property Tax Obligations

26th Jul 2023

John Marcarian

As an Australian expat living in the USA you may have to contend with the impact of taxes on property that you own in Australia or in the USA The types of taxes relating to property that you may...

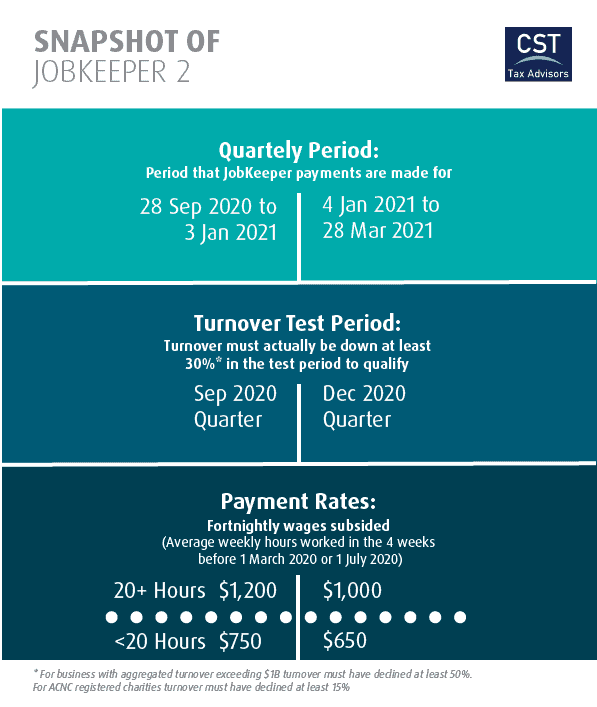

The government has announced an extension to JobKeeper beyond the initial 28 September conclusion. This extension means it is available to all eligible businesses (including the self-employed) until March 28 2021.

However, JobKeeper is not simply carrying on in its current form. Businesses who have been claiming JobKeeper subsidy may not continue to be eligible. New businesses who were not previously eligible may become eligible in the September quarter and be able to apply for the extended JobKeeper period.

Keep in mind that due to the ongoing pandemic, changes may continue to be made up to, and even beyond the time, that the new JobKeeper payments kick in.

Here’s an overview of the changes that have been announced:

Qualification Criteria

To receive JobKeeper payments after 28 September the business will have to show that their actual turnover has experienced a significant decline for the September 2020 quarter. This differs to the original requirement of simply having to have a reasonable expectation of decline.

This means that a qualifying business must actually have a turnover that, in their September 2020 quarter, is at least 30% less than the turnover they had in their September 2019 quarter.

Businesses with an aggregate annual turnover of more than $1 billion must actually have a turnover for their September 2020 quarter that is at least 50% less than their September 2019 quarter.

To continue to claim the JobKeeper payments for the March 2021 quarter, the business will have to confirm the ongoing impact of loss of income in the December 2020 quarter. This means they must actually have the lower income in the December 2020 quarter when compared to their December 2019 quarter, in order to continue to claim JobKeeper in the March 2021 quarter.

Businesses who were not previously claiming JobKeeper, but who are eligible in the September 2020 quarter based on their actual turnover, and meet all the other original qualifying tests, may apply as new recipients.

As occurred with the original JobKeeper payments, the Commissioner will have the discretion to set alternative tests, where comparing the actual turnover to the equivalent period in the prior year, is not appropriate.

Eligible Employees

Employees that will be included in the extended JobKeeper subsidy must meet the following criteria:

Currently employed by the employer (including being stood down or re-hired).

Were a full-time, part-time, of fixed-term employee at 1 July 2020 OR

Were a long-term casual who was employed for over 12 months on a regular basis, and is not employed as a permanent employee elsewhere.

Over 18 years of age on 1 July 2020 (or an independent 16 or 17 year old who was not studying full-time).

Australian resident (as defined in the Social Security Act 1991) or

New Zealand citizen living in Australia under the Special Category Subclass 444 visa (which is the Visa that automatically applies to New Zealand citizens who come into Australia).

Were not being paid parental leave or Dad and Partner pay under the Paid Parental Leave Act 2010.

Were not being paid under a worker’s compensation payment due to a total incapacity to work.

An individual who has multiple jobs can only claim JobKeeper from one employer. They cannot elect to claim JobKeeper in a position where they have been a regular casual for more than 12 months, if they are eligible for JobKeeper with another employer for whom they are permanently employed.

Self-employed individuals will be eligible to continue to receive JobKeeper as long as they meet the original requirements and the relevant turnover test, and are not permanently employed by another employer.

Payment Amount

December Quarter:

Under the extended JobKeeper payments, the fortnightly payment will be reduced from $1,500 to $1,200. This is for any employee who was employed for at least 20 hours or more a week.

For employees who worked less than 20 hours a week, payments will be reduced to $750. Business participants who worked less than 20 hours a week will also be paid at these lower rates.

March Quarter:

For the March 2021 quarter the JobKeeper payments drop to $1,000 a fortnight for all eligible employees who worked for at least 20 hours a week.

Employees who worked less than 20 hours a week will be paid out at $650 a fortnight.

The working hours used to determine whether an employee worked more or less than 20 hours a week are the 4 weeks prior to 1 March 2020. However, this test period may not always be relevant since the extension now includes permanent employees who were employed as of 1 July 2020, and casuals who meet the 12 month employment criteria by 1 July 2020.

A business may apply for the Commissioner’s discretion for alternative tests where an employee or business participant’s usual working hours were different in the qualifying period than they would normally have been (for example if they were on voluntary leave during the bushfires, or not employed in the previous quarter).

Further Information About JobKeeper

Like the original JobKeeper program, JobKeeper is a wage subsidy that is paid to eligible employers in order to help cover the cost of wages that they are paying to their employees.

The JobKeeper income received counts as taxable income to the business, just as the wage payments made count as a tax deductible expense to the business. Any JobKeeper payments made to the business via claims based on an eligible business participant are also included as taxable income for the business. There is no GST on this income and it does not count as turnover for GST purposes.

The Treasury’s fact sheet on the JobKeeper extension can be found here.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

Key tax differences between a Permanent Resident and Temporary Resident

Daniel Wilkie | 20 Aug 2020 | 4 min read

The rules around tax residency are largely different to the rules around social security, visa residency, as well as citizenship.

Australian Tax Resident

In Australia, for tax purposes, an individual is an Australian resident if they satisfy one of the residency tests.

However, those people from outside of Australia may not realise that establishing that you are an Australian tax resident is not the end of the story. An Australian tax resident may be a permanent resident or a temporary resident, with different tax implications.

Temporary Australian Tax Resident

A temporary Australian tax resident is an Australian resident who:

Holds a temporary visa under the Migration Act 1958

Is not an Australian resident according to the Social Security Act 1991

Does not have a spouse who is an Australian resident within the meaning of the Social Security Act 1991

The Social Security Act 1991 defines an ‘Australian resident’ as a person who resides in Australia and is an Australian citizen, holder of a permanent visa or a protected special category visa holder.

As you can see this is different to the tax definition of Australian tax resident.

Temporary residents may be considered an Australian tax resident due to a “permanence” in their intention and action of residing in Australia, however, they may not be legally allowed to permanently reside in Australia based on their Visa, which means they will likely return to their home country.

(NZ citizens are a special case, where they can remain in Australia without applying for permanent residency, but are still considered Temporary Residents based on the “Special Category Visas” issued to them upon entry to Australia.)

The Difference Between a Temporary Resident and a Permanent Resident for Tax Purposes

All Australian residents are taxed on their Australian and worldwide income, including any capital gains on foreign property held.

Foreign residents are taxed only on their Australian sourced income.

Permanent Australian residents are treated the same as an Australian resident, and taxed on both Australian and worldwide income.

Temporary residents are taxed on their Australian-sourced income only. They are taxed at resident marginal tax rates, however, they do not pay tax in Australia on their foreign-sourced income.

Foreign residents and temporary residents are subject to capital gains tax (CGT) if a CGT event happens to a CGT asset that is taxable Australian property. They are not subject to CGT in Australia on their foreign owned taxable property for CGT purposes. This ensures, for example, that they can reside in Australia on a temporary basis without having to worry about the CGT consequences of a home they maintain back in the country in which they permanently live and are likely to eventually return to.

Taxable Australian Property

‘Taxable Australian property’ are capital assets that include real property situated in Australia, mining rights in Australia, assets of a business located in Australia, and indirect interest in Australian real property through an entity that you hold 10% or more controlling interest in (where such interest is primarily associated with ownership of the Australian real property).

This also includes options over any of the above.

Individuals are taxed on any taxable Australian property, regardless of their residency status.

Overview of Different Tax Treatment

Non-Resident

Temporary Resident

Permanent Resident

Taxed on overseas income

NO

NO

YES

Taxed on Australian sourced Income

YES

YES

YES

CGT on taxable Australian property

YES

YES

YES

CGT on foreign taxable property

NO

NO

YES

Entitled to claim CGT main residence exemption on Australian main residence

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Exceptionally talented individuals with the capacity to raise Australia’s standing in their field may be eligible for a Global Talent Visa This Visa is a permanent residency Visa that offers a...

When you live and work solely in one country, tax residency is straightforward However, if you are living away from your home country or living between multiple countries, then determining tax...

Technology and Pandemic Create Tax Issues for Foreign Employees and Foreign Companies

Daniel Wilkie | 16 Jul 2020 | 3 min read

Advancing technology is rapidly bringing possibilities to the workforce that once seemed to be nothing but science fiction. AI (artificial intelligence), virtual reality, data communications, augmented reality, and more sophisticated automations are already making their mark to various degrees.

In addition, the COVID19 pandemic has seen hundreds of thousands of Australians return from abroad. Many of those returning may be able to continue working for their foreign employers.

What does this all mean?

With the rise of the internet and global e-connectivity many organisations in finance, information technology, telecommunications and professional services had been realising that their employees did not have to be physically present in the workplace to perform their job function.

Even before the pandemic that trend had well and

truly commenced. The enormous outsourcing industry has been a testament to

that. The necessity of lockdowns should accelerate that trend.

Working for foreign employers from Australia

An increasing number of Australians will be able to take advantage of continuing permanent employment opportunities, not with domestic employers but with overseas employers.

When you are a tax resident in one country, but your sole source of income is from another country, you may find that not only do you face double the tax administration, but if the correct advice is not taken you may face higher effective rates of taxation.

As more of these scenarios emerge, there will be a need to obtain tax advice from advisors who are experienced with addressing these issues.

Corporate tax laws stem from over one hundred years of legal history and they are not about to change any time soon to accommodate modern times. Australia’s laws around corporate residency are well understood and the reality is that if you are a controlling director of a foreign company and you have returned to Australia, you should seek tax advice in relation to how Australia’s tax laws apply to foreign companies.

The consequence of not seeking detailed advice is that the foreign company in question might be a resident of Australia and its profits might be subject to Australian corporate tax depending on the situation.

If you are a controlling shareholder of a foreign company, you might also find that Australia’s tax laws will attribute some or all of the company’s profits to you even if a dividend is not paid to you. This outcome can arise depending on the facts, because of Australia’s Controlled Foreign Company rules.

Changing the way you interact with your accountant

If you are working for a foreign employer from Australia, there will be a need for income tax advice to ensure that you properly plan for tax outcomes and are not caught out with unexpected tax bills.

Keeping in touch with your accountant more

regularly to plan your position will be increasingly important if you find

yourself in this situation.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

OECD Guidance on Potential Tax Consequences of COVID-19 Work and Travel Restrictions Keeping Australians Overseas

Daniel Wilkie | 14 May 2020 | 6 min read

For many businesses, investors, and travellers, international travel is a regular, or important part of life. When 2020 started there were only very vague whispers that something was lurking over in China. Otherwise, travel, and travel plans, went on as usual. However, things very quickly escalated as COVID-19 began to spread around the world, with country after country swiftly and suddenly imposing international travel bans and local movement restrictions.

From a tax perspective this does lead to the question of what tax consequences arise in these situations.

OECD Guidance

The OECD has released some guidance on what this could mean from a tax perspective. The following notes are based on the 3 April 2020 version of this advice.

Unintentional Creation of a “Permanent establishment” for Businesses Through Employees Stranded Overseas

It is considered unlikely that individuals who have been dislocated overseas and are working from a residence overseas during this crisis, will be seen as creating a permanent business establishment overseas. This is an exceptional situation where employees may temporarily be working in a different location for a long time.

In general, an isolated individual who is required to work from an overseas home is only working there on intermittent business activities and not creating a place of business that is used on a continuous basis to carry out the tasks of an enterprise. The situation is out of the control of the business, where the normal place of work is inaccessible.

However, it is also important to consider the domestic laws in the country where an employee is working during this time. Domestic laws may have different requirements in place, may not be adequately covered by a double tax treaty, or may not have legislated exemptions specific to the COVID-19 travel restrictions. It is therefore important to obtain advice specific to the country in which an employee is working during the COVID-19 travel restrictions.

It is also important to note that if an employee was habitually concluding contracts overseas on behalf of the business back in their home country, before COVID-19 travel restrictions were imposed, that they may be treated differently for tax purposes.

Could the Residence Status of a Company be Impacted when the Effective Place of Management has been Displaced Overseas During COVID-19 Travel Restrictions?

Some businesses may have found that their chief executive officers or other senior executives are stuck in a country other than the company’s country of residence, for the duration of the COVID-19 restrictions. This leaves those businesses concerned that there is effectively a relocation of management to an overseas location, which could in turn impact the company’s tax residency status.

Again the advice noted is that it is unlikely that situations created by COVID-19 restrictions will cause an unintended change in an entity’s status for tax residency. This is because the change in location of management is both an extraordinary and temporary situation due to an emergency situation.

Tax treaties typically contain tie breaker rules that should ensure this remains the case. In particular it is noted that the key to determining the location of management is the place where management usually occurs. This means a forced change of location of management during COVID-19 travel restrictions is unusual and exceptional, as well as temporary, in that the intention will be to resume usual operations once the travel restrictions are lifted.

Cross Border Workers

When a government is subsidising the wages of an employee who usually works in one location but is being paid while simply residing in another, from which country would this income be attributable?

The OECD Commentary indicates that this should be the place where the employee would otherwise have been working to earn their usual wages. This is because taxing rights are typically given to the place where employment duties are performed. Since the government payment is in relation to their normal employment duties, normal taxing rights apply to the source country. The country of residence would therefore be required to tax this income under the usual double taxation relief between the two countries.

Change of Residence Concerns

The OECD indicates that it is unlikely that the COVID-19 situation will affect the normal treaty residence position.

Australia, the UK, and Ireland, for example, have all issued guidance making it clear that where it is merely the exceptional circumstances of COVID-19 travel restrictions that are keeping non-residents within the country, this will not cause a change in tax residence.

However, it should be noted that such guidance has been qualified. For example, it is the ATO’s view that if a temporary change due to COVID-19 becomes permanent, then all the usual income tax issues will need to be confronted.

Business as Usual

In general it appears that the OECD is suggesting that COVID-19 travel restrictions will not, by and large, result in changes to the usual measures and tax treatments that are in place.

This is because the COVID-19 restrictions are government mandated restrictions that are out of the control of the businesses and individuals who are impacted by them. They are exceptional circumstances imposed to deal with an emergency situation, rather than business as usual, and they will therefore only be temporary measures, even if they last for a lengthy period.

It should, however, be noted that all of these indications are general in nature and largely based on the model double taxation conventions as well as typical responses around the world to the COVID-19 travel restrictions and the way different countries are dealing with the issues that have arisen from this.

Specific tax advice should be sought from the local jurisdiction in which you are residing whilst under COVID-19 travel bans, as well as your Australian international tax specialists, to ensure that your specific situation, and the applicable double tax agreement and extraordinary circumstances are properly understood.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

With legislation rapidly being implemented there have been a lot of unanswered questions surrounding the JobKeeper wage subsidy. On April 8 2020 the Federal Government passed the package and the Bill received Royal Assent on April 9 2020.

The Treasury continues to release clarification of issues surrounding the JobKeeper payment based on this legislation. Here are some of the key clarifications to help you work out how JobKeeper might work for your business.

Table of relevant dates for the first months of the scheme

JobKeeper Fortnight Ending

Must be registered by this date to qualify for reimbursement of this period

Date that the business must pay the minimum $1,500 to the employee by

ATO schedule to be pay reimbursements to the business from

12 April 2020

26 April 2020

30 April 2020

14 May 2020

26 April 2020

26 April 2020

30 April 2020

14 May 2020

10 May 2020

10 May 2020

10 May 2020

End of May 2020

24 May 2020

24 May 2020

24 May 2020

End of May 2020

7 June 2020

7 June 2020

7 June 2020

End of June 2020

21 June 2020

21 June 2020

21 June 2020

End of June 2020

Overview of the JobKeeper Payment

In essence the JobKeeper payment is a wage subsidy for employers who have suffered a loss of income of least 30% of their business turnover. (Or at least 50% loss where the turnover exceeds 1 billion).

Eligible employees are paid a minimum of $1,500 a fortnight through their usual payroll and the government will reimburse the business a fixed amount of $1,500 per fortnight per employee.

For a more detailed explanation on this, including who is eligible, please see our previous post on the JobKeeper package.

Given the sudden announcement of the JobKeeper package there were a lot of unanswered questions. Many of these have now been clarified.

How do I know if my turnover has dropped enough?

The government initially indicated that your decline should be measured by comparing your usual period of trading to the current period of trading. For example the March month this year compared to the March month last year.

They then gave the Commissioner of Taxation the power to issue alternative tests when this did not provide a reasonable assessment of the situation that the business faces, or where the business had not been in operation for at least 12 months.

While it is still not 100% clear how this will work in practice, here is what we do know:

Turnover and eligibility is measured on a self-assessment basis, using both historical figures and reasonable estimates.

The ATO has the power to administer tests and provide guidelines on how to make these measures. They will be releasing more guidance on this.

The Commissioner of Taxation also has discretion to apply some flexibility to the measures.

Businesses will be required to report their monthly eligibility to the ATO.

The ATO has confirmed that the following in an update on the ATO’s website of 17 April 2020;

“If you work out that you qualify for the JobKeeper payments for the first fortnight because your turnover has declined by the relevant amount, you remain eligible and do not need to keep testing turnover in following months. However, you will have ongoing monthly reporting requirements. More information will be provided soon. (our emphasis added).

The Commissioner of Taxation also has the discretion to set out alternative tests that can establish your eligibility when turnover periods are not appropriately comparable (for example, if your business has been in operation less than a year). We will provide more information soon about alternative tests.”

Applying for the JobKeeper subsidy

The JobKeeper subsidy is not automatic. You must register for the scheme to receive the wage subsidy.

This was initially done by registering your interest in the program with the ATO through their online form. Note that this is just registering an interest in applying and is not actually the formal application itself.

From 20 April 2020 tax agents will be able to enrol their clients in the JobKeeper Payment Scheme using the ATO’s Online services.

You cannot retrospectively register for the JobKeeper payment in the future. You must be registered under the scheme before the end of any relevant JobKeeper fortnightly payment. Since this is not possible for the first applicable fortnight, this applies to all relevant fortnights except the first one, for which you must be registered by April 26.

In effect this means if you wish to apply for the JobKeeper subsidy from the first possible fortnight then you need to ensure you are enrolled within days of enrolment being open.

If your turnover was not initially impacted by the coronavirus but is, or you expect it will be, as the months progress, then you can register during the first applicable fortnight to commence JobKeeper payments from that fortnight.

Once you register you remain registered and report monthly to confirm ongoing eligibility. The scheme is expected to go on for a total of six months.

Clarification on who is an eligible employee and whether the business can choose who to enrol

If a business enrols in the JobKeeper program they are required to include ALL eligible employees. This means they can’t refuse to include selected employees from the scheme if that employee is eligible to be included.

An employee is an eligible employee if they:

Are at least 16 years of age.

Are an Australian resident for social security purposes or a Subclass 444 (Special Category) visa holder who is a resident of Australia for tax purposes (this effectively covers all NZ citizens who came to Australia on a NZ passport).

Are a fulltime or part-time employee, OR they are a casual who has worked with the business on a regular and systematic basis for at least 12 months, and the casual has no other place where they are permanently employed. This means a long-term casual cannot be included if they are a fulltime or part-time worker elsewhere, even if their other employer is not able to enrol in the JobKeeper scheme.

Are not being paid government funded parental leave pay, dad or partner pay, not being fully supported through a worker’s compensation scheme.

In addition the eligible employee:

Must not have been given notice by any other employer that they are enrolled in the JobKeeper scheme with them. (An individual employee can only be covered by one employer).

They must complete a JobKeeper employee nomination notice.

How Much Are Employees Paid under the JobKeeper Scheme?

All eligible employees must be paid a minimum of $1,500 a fortnight by an employer who is enrolled in the JobKeeper scheme.

Where an employee is usually paid more than this, the employer should simply continue to pay the employee their usual wages. For situations where the employee is usually paid less than this, the employer is required to top up the employee’s wages to $1,500 for every eligible JobKeeper fortnight.

If an employee had been stood down after March 1 2020 then the business should now pay the minimum of $1,500 a fortnight to the employee in order to be reimbursed. There is no requirement for an employee to be paid more than this in this situation, even if their normal rate of pay of was higher than $1,500 a fortnight.

When an employee ceased employment after March 1 2020 they can be rehired under the JobKeeper scheme. If they were paid out a redundancy pay, this will need to be sorted out.

When must JobKeeper Payments be made to the employees?

To be eligible for the JobKeeper wage subsidy you must make the minimum $1,500 payments by the end of the fortnight for which you are claiming.

This means if an employee is normally paid monthly you are required to split the payment so that the employee is actually paid at least their JobKeeper rate for each JobKeeper fortnight.

There is an exception for the first two fortnights. These must be paid by the end of April 2020. This gives employees room to adjust payments for eligible employees for the month that they were sorting out eligibility and waiting on legislation.

Does my employee actually have to work a minimum amount to be paid under the JobKeeper program or can my employee refuse to work while being paid under the JobKeeper scheme?

If your employee cannot be usefully employed during their normal hours of work for the relevant fortnight, then they can stand down for part or all of the fortnight that they are paid the JobKeeper payment. This does not mean that employees can elect not to work. If they are still able to work, even in a reduced capacity, from home instead of at the business premises, or in any other such way as the business can arrange, then they should still continue to work for their employer.

By the same token an employer cannot use enrolment in this scheme as an opportunity to reduce a staff member’s normal hourly rate of pay.

In effect this means that all eligible employees should be paid either the greater of their normal pay for the hours actually worked or the JobKeeper amount, which may be a payment while they are standing down or include a top up above payment for the actual hours worked.

Is Superannuation Payable on the JobKeeper payment?

Superannuation is still required as normal on any component of wages that are paid under normal employment conditions. Any component of the $1,500 payment made to eligible employees that is purely a top up to the JobKeeper rate has no superannuation requirement attached. This is because they are not actually working for that component of their wage.

For example:

Jack is an eligible employer who employs Jill. Jill is an eligible employee who normally works part time and is paid $1,000 a fortnight. For the relevant JobKeeper fortnights Jack is required to pay Jill a higher amount of $1,500 a fortnight.

Jack is still required to pay superannuation on $1,000 of each pay, since this is simply Jill being paid her normal wage for the work performed. Jack is not required to pay Superannuation on the additional $500 top up amount that is paid to Jill.

Are Fair Work Conditions Affected By The JobKeeper Scheme?

Amendments have been made to the Fair Work Act 2009 to ensure that the JobKeeper Scheme can work in practice and businesses can adjust their working arrangements to situations that are more flexible and suitable for this time. The basic rights and responsibilities of employees and employers continue, there is just room for flexibility to facilitate the continuation of business operations during the unprecedented restrictions that apply due to the coronavirus.

No adjustments to an employee’s requirements can be used to reduce their base hourly rate of pay. This includes requiring them to work from home or adjusting the tasks that they perform so that they are duties that can be carried out from home. An employee can only be required to work at an alternative place of work if the new work location does not require them to travel an unreasonable distance, in the specific circumstances of the business, from their home.

During the period for which an employer is eligible for JobKeeper they can enter into arrangements with their employees that are different to their normal employment arrangements. This allows an employer to ask their employee to work on different days or times than usual based on the adjusted needs during the coronavirus. This does not allow the employer to reduce the employee’s working hours where there is no reason to.

Employers are also allowed to ask employees to take annual leave (including at half pay) for this period, as long as this will not result in the employee’s leave balance reducing to less than two weeks.

Business participants: Claiming JobKeeper as a Business Owner

Although we are still waiting on further clarification in regards to how business owners can claim JobKeeper there are a few points that have been released. Perhaps the most important one to note is that only 1 business owner can claim the JobKeeper payments from the business, regardless of how many business owners there are.

Sole traders, partners in a partnership, directors or shareholders of a company, or an adult beneficiary of a trust, are all eligible business participants for the JobKeeper scheme if they are actively engaged in running the business.

These are the important things to note so far:

Business owners who are eligible business participants can also claim JobKeeper payments for themselves if their business meets the eligibility requirements.

Even if there are more than 1 eligible business participants in a business, only one individual can be nominated to receive the JobKeeper payment. This means, for example, a partnership entity can only nominate one partner to receive the JobKeeper payments.

The business must have had an ABN on or before 12 March 2020 to be eligible (unless the Commissioner allows a later time at their discretion).

The relevant business participant must not be elsewhere eligible for the JobKeeper payment, either as an eligible employee elsewhere, or as a nominated eligible business participant for another business.

This means if an individual is eligible as an employee elsewhere that they cannot be a nominated business participant. If they are employed as a casual elsewhere then they can choose between the casual role or the business as their source of JobKeeper payments. Where an individual could be an eligible business participant in multiple businesses they can only be nominated for one of those businesses.

All individuals are only entitled to receive JobKeeper from one source. All businesses are only entitled to claim JobKeeper for one business owner.

There is not yet a formal application process available for eligible business participants.

Does the decline in turnover test need to be met on an ongoing basis?

It now appears that once a business has satisfied the decline in turnover test they can enrol for JobKeeper Payments. Once they are enrolled in the scheme they will continue to be eligible so long as they continue to pay their eligible employees through the scheme.

Does the business have to enrol in the JobKeeper scheme from the start?

No. If the business doesn’t initially meet the requirements it can later enrol in the JobKeeper program if they satisfy the decline in turnover tests (and fulfill other eligibility criteria) at a later date.

In Summary

If you wish to apply for the JobKeeper scheme for your business and be eligible for the wage subsidy from the start of the scheme, you will need to enrol and ensure your eligible employees are all confirmed and have been paid their minimum required payments no later than the end of April 2020.

If your business does not become eligible until a later date then you can apply for the JobKeeper scheme from that point in time.

Further clarifications will continue to be provided as the government, and the ATO sort through the processes.

Written by Daniel Wilkie

Daniel has over 15 years of experience providing taxation services to family groups, businesses and individuals. Having lived and worked abroad, Daniel understands what is involved when making a move overseas. Daniel’s main areas of expertise include superannuation, employee share schemes, companies and family trusts.

While details contained in this article are accurate at the time of publication, they may be subject to changes in statutory and case law as well as Government policy, rulings and interpretation updates. Any opinions expressed are those of the writer and may no be representative of the CST firm or applicable under different circumstances. Any advice contained herein is generic in nature only and cannot be relied on for your personal situation. As such we cannot be held responsible for any damages that arise from applying generic information to your own situation. You should always seek professional advice tailored to your unique situation, taking into account the most recent legal changes and understandings at the relevant time.

Use our online tool to determine the corporate residency of your client's business.

Contact Us

"*" indicates required fields

More articles like this

Tax Implications Of 401(k) And IRA Plans For Australian Tax Residents

9th Apr 2024

Matthew Marcarian

Retirement savings, especially when managing finances across international borders, can be complex If you live in Australia, but hold plans in the USA, you need to understand the tax implications of...

Our principal, Matthew Marcarian, was recently published in Australia’s leading tax journal, Taxation in Australia (run by the Tax Institute), with his article titled “Australian Expatriates:...

Tax obligations for Australians working on Super Yachts

21st Jun 2022

Matthew Marcarian

For Australians interested in travel, one of the appeals of working on a super yacht or cruise ship could be the idea that their income becomes tax-free once they leave AustraliaUnfortunately...

Commercial Rent Relief For COVID-19 Impacted Small Business Tenants

Daniel Wilkie | 9 Apr 2020 | 12 min read

On April 7 2020 the government announced another stage of coronavirus economic support. This announcement was for commercial tenants who are affected by coronavirus. Many businesses have had to close their doors or operate at significantly reduced levels of sales at this time. These measures, combined with the previously announced economic packages, are designed to help many of these businesses survive this unprecedented crisis and lessen the overall economic impact from the pandemic.

Who is Eligible to Claim Commercial Rent Relief?

There are two criteria that must be satisfied for a commercial tenant to be eligible for the rental reductions.

The business must have a turnover of $50 million or less

The business tenant must be eligible for and have applied for JobKeeper support

Summary of the Essential Components of Commercial Rent Relief:

The following applies to eligible tenants, for so long as the pandemic lasts and for a reasonable recovery period afterwards:

Landlords cannot evict tenants for non-payment of rent.

Rental prices cannot be increased (unless the lease agreement is based on a set percentage of business turnover and accordingly already fluctuates with business turnover).

Any savings on lease outgoings (council rate, land tax, insurance reductions etc) should be passed on to tenants.

A landlord must reduce the lease payments by at least the same percentage as the business’ turnover has reduced. This means if a business has lost 100% of their income their rental payment requirements are reduced by 100%. If a business has lost 50% of their income their rental payment requirements must be dropped at least 50%.

50% of the rental reductions must be waived completely. Where a tenant’s business will unduly suffer if only 50% of their rental is waived, then the landlord is required to waive a higher proportion of the rental.